Stated Income Loans: Rates and Terms for Self Employed

What Today's "Stated Income" Loans Actually Are

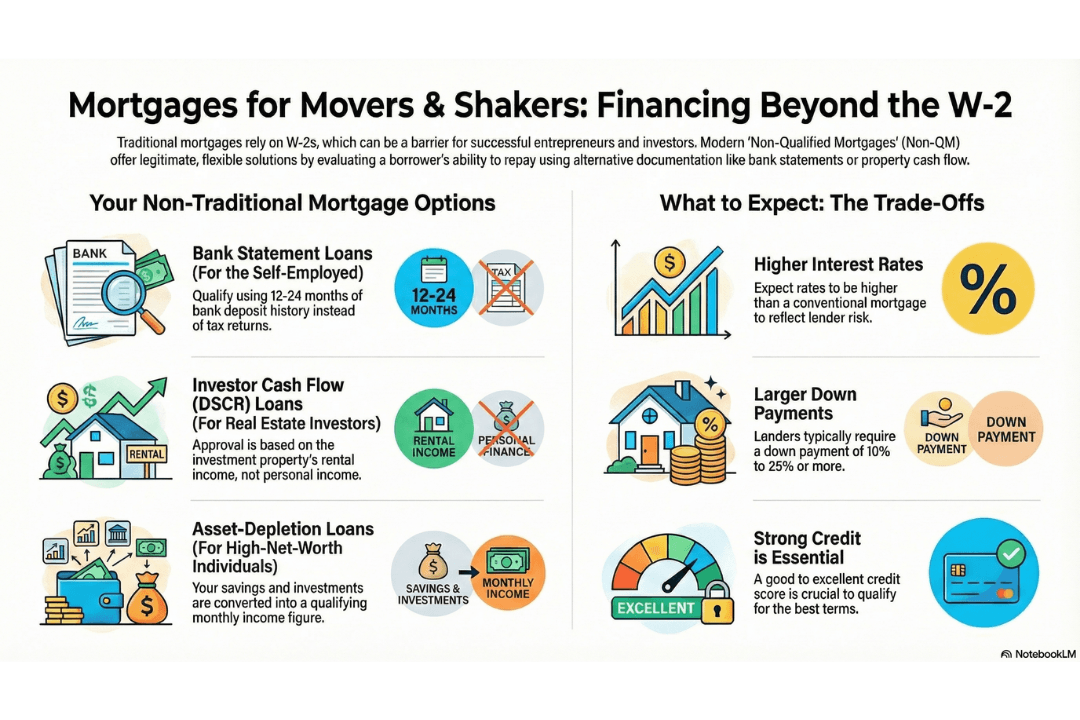

The loans often marketed today under the "stated income" umbrella are known as Non-Qualified Mortgages (Non-QM), and they are legitimate, responsible products designed to assess a borrower's ability to repay through non-traditional means. The most common types include:

1. Bank Statement Loans (The Modern Default)

This is the closest equivalent to what most self-employed borrowers seek.

How it Works: Instead of W-2s and tax returns, the lender analyzes 12 to 24 months of the borrower's personal or business bank statements.

The Benefit: This is ideal for entrepreneurs, freelancers, and small business owners who utilize aggressive tax write-offs (deductions) to legally minimize their taxable income. Since lenders base qualification on the actual cash flow (deposits) shown in the bank, the low net income reported on tax returns becomes irrelevant. Lenders will typically apply an "expense factor" (e.g., qualifying on 5%-50% of deposits) to account for business costs which is normally backed by a CPA or tax-preparer's letter.

2. Investor Cash Flow (DSCR) Loans

This product is specifically designed for real estate investors purchasing rental properties.

How it Works: The loan qualifies based on the investment property's potential to generate rental income, not the investor's personal income. The lender calculates the Debt Service Coverage Ratio (DSCR):

DSCR = Gross Monthly Rent / Monthly Mortgage Payment (PITI)

The Benefit: If the DSCR is greater than 1.0 (meaning the rent covers the mortgage payment), that's a great starting point for a qualifying ratio. We will allow ratios under 1.0 also which makes it helpful when the rental income is below the full PITI payment. This allows investors to expand their portfolios without having to show a massive personal income or adding complexity to their personal tax returns.

No Current Renter: The property does NOT need to be occupied to establish a rental income ratio calculation. The appraisal will include what's called a "market rents" analysis and will establish what that rental rate figure should be for the property.

3. Asset-Depletion Loans

How it Works: This option is for high-net-worth individuals, often retirees, who have substantial liquid assets (savings, investment portfolios, retirement accounts) but little traditional income. The lender calculates a qualifying monthly income by dividing the total liquid assets by a fixed number of months (e.g., 60 to 360 months).

The Benefit: It allows those with a strong net worth but low reportable income to qualify for a mortgage based on their overall financial stability.

Why These Loans are a Game-Changer

For the Self-Employed Borrower: They allow successful entrepreneurs to separate their tax strategy (minimizing taxable income) from their mortgage qualification strategy (showing ample cash flow). This enables them to buy their dream home or a new property, a goal often blocked by conventional lending rules.

For the Investor: DSCR and other alternative docs allow for rapid portfolio scaling. An investor can acquire properties quickly, qualifying each new property based on its own income potential, making the process faster and less cumbersome than constantly having to prove their personal income stability.

The Cost and Key Considerations

While modern stated income alternatives offer incredible flexibility, they are priced to reflect the increased risk the lender takes on by not using standard documentation.

Higher Interest Rates: Expect the interest rate to be higher than a conventional (Fannie Mae/Freddie Mac) mortgage.

Larger Down Payments: Lenders typically require a larger down payment (often 10% to 25% or more) to mitigate risk.

Stronger Credit: A good to excellent credit score is usually essential to qualify for the best terms.

While modern stated income alternatives offer incredible flexibility, they are priced to reflect the increased risk the lender takes on by not using standard documentation.

Higher Interest Rates: Expect the interest rate to be higher than a conventional (Fannie Mae/Freddie Mac) mortgage.

Larger Down Payments: Lenders typically require a larger down payment (often 10% to 25% or more) to mitigate risk.

Stronger Credit: A good to excellent credit score is usually essential to qualify for the best terms.

Other Alternatives for Non-Traditional Income

While modern stated income alternatives offer incredible flexibility, they are priced to reflect the increased risk the lender takes on by not using standard documentation.

Higher Interest Rates: Expect the interest rate to be higher than a conventional (Fannie Mae/Freddie Mac) mortgage.

Larger Down Payments: Lenders typically require a larger down payment (often 10% to 25% or more) to mitigate risk.

Stronger Credit: A good to excellent credit score is usually essential to qualify for the best terms.

If a Non-QM loan isn't the right fit, self-employed borrowers and investors still have options:

The takeaway is simple: the financial world has evolved. Being self-employed or a dedicated investor no longer means being shut out of the best financing opportunities. By understanding the modern alternatives to the old "stated income" loan, you can find a financial solution that truly reflects your entrepreneurial success and cash flow.

MORTGAGE ARTICLES

133 E. De La Guerra St. #59

Santa Barbara, CA 93101

Email: loans@mortgagewholesale.com

805-419-3319

NMLS: 380097

Copyright © 2025 Mortgage Wholesale - All Rights Reserved