Jumbo Mortgage Loans: Best Rates and Requirements for Self Employed

🚀 Jumbo Loans for the Self-Employed: Your Guide to Non-QM Financing

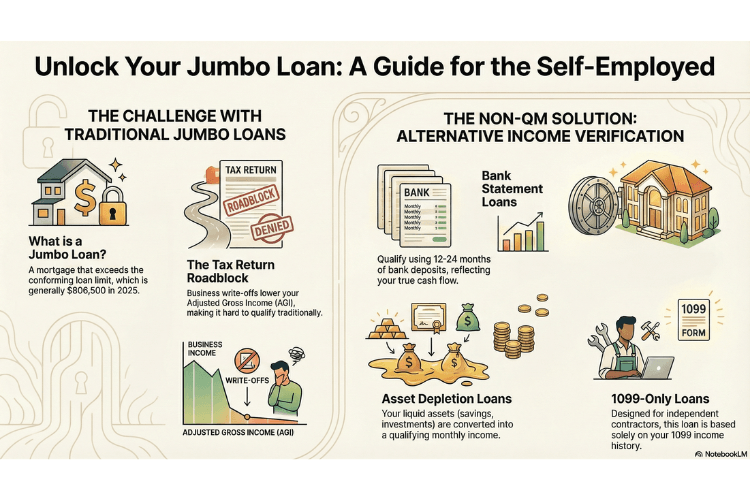

Being your own boss comes with a host of advantages, but when it comes to getting a large mortgage, the traditional path can feel like hitting a roadblock. If you're a high-earning, self-employed individual needing a Jumbo Mortgage Loan—a loan that exceeds the conforming loan limits (generally $806,500 in 2025, higher in high-cost areas)—your financial structure can make standard qualification tricky.

The good news? The rise of Non-Qualified Mortgages (Non-QM) has opened up flexible, powerful financing options that look beyond your tax returns to see your true financial strength.

💰 Understanding Jumbo Mortgage Rates and Requirements

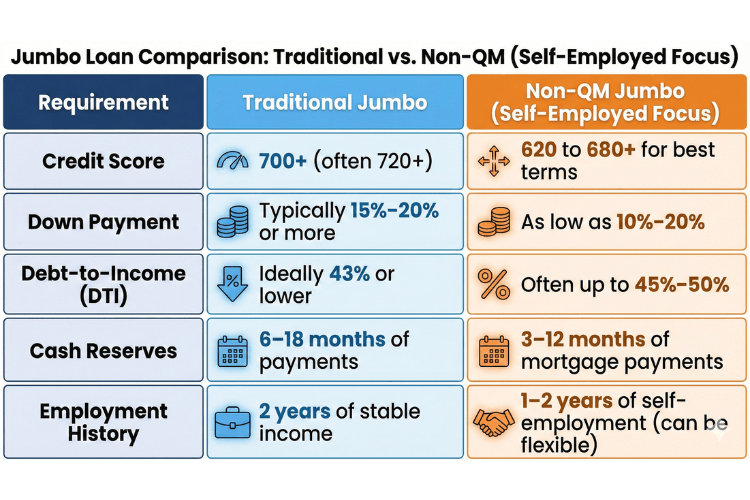

Jumbo loans are considered riskier by lenders because they are not backed by government-sponsored entities like Fannie Mae or Freddie Mac. For a self-employed borrower, this translates into more stringent requirements than a standard loan.

📊 Key Qualification Requirements for a Self-Employed Jumbo Loan:

📈 Current Rate Landscape

Jumbo loan rates tend to follow the same market trends as conforming loans, but they are often slightly higher due to the increased risk. As of late 2025, 30-year fixed jumbo rates are typically ranging from 6.0% to 7.0% or more, depending heavily on your credit profile, reserves, and the specific loan product.

Pro-Tip: Consider a Jumbo ARM (Adjustable-Rate Mortgage), such as a 5/6 or 7/6 ARM, which may offer a lower introductory rate for a fixed period. This can be appealing if you don't plan to keep the loan long-term.

🏦 Best Jumbo Loans for the Self-Employed: The Power of Non-QM

The challenge for many self-employed individuals is the amount they write off on their tax returns. While smart for business, these deductions can drastically lower your Adjusted Gross Income (AGI), making it difficult to qualify for a traditional loan.

Non-QM jumbo loans solve this by using alternative income documentation. Here are the top programs tailored for you:

1. Bank Statement Loans

This is the most popular Non-QM option for the self-employed.

How it works: Instead of tax returns, the lender analyzes 12 or 24 months of your personal or business bank statements. They calculate your average monthly deposits to determine your qualifying income.

Why it's great: It gives you credit for your true cash flow, ignoring the depreciation and business write-offs that reduce your taxable income.

2. Asset Depletion Loans

Ideal for high-net-worth individuals with substantial liquid assets.

How it works: The lender calculates a qualifying income by dividing your total verifiable assets (savings, investments, retirement accounts) over a fixed number of months (e.g., 60 to 360 months).

Why it's great: You can qualify based on your wealth without needing high W-2 or bank statement income, and you generally do not need to liquidate your assets.

3. 1099-Only Loans

Specifically designed for independent contractors, freelancers, and others who receive 1099 income.

How it works: The loan is based solely on your 1099 income documentation, often requiring 1 or 2 years of history.

Why it's great: It simplifies the process for independent workers who don't have business bank accounts or traditional business structures.

🏡 What Types of Property Will Non-QM Loans Refinance?

Non-QM Jumbo loan programs are highly flexible and are used for both purchases and refinances, often covering a wider range of property types than conventional loans.

For a self-employed borrower seeking a refinance (including cash-out or rate-and-term), Non-QM jumbo lenders will typically work with:

Primary Residences (Owner-Occupied): Single-family homes, townhomes, and certain condominiums and also non-warrantable condos.

Second Homes/Vacation Homes: Properties that are non-owner-occupied but used by the borrower for leisure.

Investment Properties (Non-Owner Occupied): Including single-family homes, multi-unit properties (2-4 units), and some unique investment vehicles.

Non-QM Flexibility for Refinances:

Many Non-QM programs are also used to refinance properties that would be considered "non-warrantable" by conventional lenders, such as:

Non-Warrantable Condos: Condominium projects that may not meet conventional guidelines due to factors like high commercial space ratios, concentration of ownership, or high delinquency rates.

Condotels: Units within a building that operates as a combination of a condo and a hotel, allowing for short-term rentals.

Multi-Family Properties: Loans on 2-4 unit properties for investors.

In summary, the self-employed no longer need to struggle with the traditional, rigid box of mortgage underwriting. Non-QM jumbo loans—especially the popular Bank Statement and Asset Depletion programs—offer powerful, flexible pathways to purchase or refinance your high-value property by focusing on your actual cash flow and financial strength.

MORTGAGE ARTICLES

133 E. De La Guerra St. #59

Santa Barbara, CA 93101

Email: loans@mortgagewholesale.com

805-419-3319

NMLS: 380097

Copyright © 2025 Mortgage Wholesale - All Rights Reserved