DSCR Loans: No Income Verification for Real Estate Investors

💸 DSCR Loans: No Income Verification for Real Estate Investors

For real estate investors, especially those who are self-employed, own multiple businesses, or simply carry a high personal debt-to-income (DTI) ratio, traditional mortgage underwriting can be a major roadblock to portfolio expansion.

Enter the Debt Service Coverage Ratio (DSCR) Loan. This powerful financing tool is a game-changer because it allows investors to qualify for a mortgage based on the property's potential income, not their personal income.

If you're looking to scale your portfolio without the burden of tax returns, W-2s, and complex personal income documentation, the DSCR loan could be your ultimate financial ally.

🔍 What is a DSCR Loan?

A DSCR loan is a type of Non-Qualified Mortgage (Non-QM) specifically designed for investment properties. Unlike conventional loans, which require lenders to calculate your personal DTI ratio using tax returns, a DSCR loan focuses entirely on the property itself.

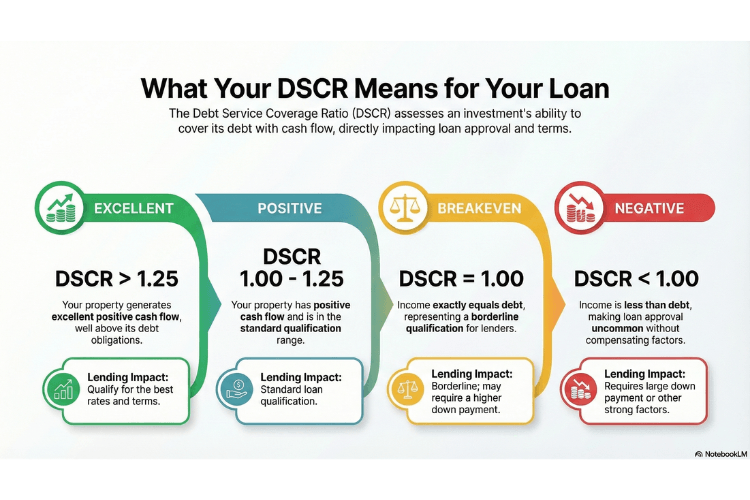

DSCR stands for Debt Service Coverage Ratio. It is a formula used to measure the property's ability to generate enough rental income to cover its mortgage debt. The ratio is calculated by dividing the property's gross monthly rent by its total monthly debt obligations (PITIA):

DSCR=PITIA (Principal, Interest, Taxes, Insurance, Association Dues)Gross Monthly Rental Income

The Magic Number: DSCR Ratio Explained

The DSCR ratio is the primary factor in loan approval and pricing:

The higher your DSCR, the lower the risk is to the lender, which generally translates to better interest rates for you.

✅ Why DSCR Loans are Ideal for Real Estate Investors

The core appeal of a DSCR loan lies in its unique flexibility, which solves common problems faced by investors:

1. No Personal Income Verification

This is the single greatest advantage. Lenders do not require pay stubs, W-2s, or personal tax returns. This is perfect for:

Self-Employed Individuals: Who take legitimate business deductions that lower their taxable income, making them unable to qualify for conventional loans.

High-Volume Investors: Who want to scale their portfolio rapidly without constantly submitting complex personal financials.

New Investors: Who may have irregular or hard-to-document income streams.

2. No Personal DTI Limitations

Since the lender only cares about the property's cash flow, your personal debts (like car loans, credit cards, or existing mortgages) do not restrict your ability to take on new debt. This allows investors to scale their property count without hitting the conventional loan limit (typically 10 financed properties).

3. Borrowing in a Business Entity

DSCR loans allow the property to be vested in an LLC, S-Corp, or Trust. This is a massive benefit for asset protection, tax planning, and liability shielding, which is a foundational strategy for serious real estate investors.

4. Flexible Property Types

These loans are highly versatile and can be used for:

Single-Family Residences (SFR)

2-4 Unit Multi-Family Properties

Condos and Townhomes

Short-Term Rentals (Airbnb/VRBO): Many DSCR lenders accept projected rental income from third-party analyses (like AirDNA) or historical rental history.

📋 Key Requirements to Qualify for a DSCR Loan

While the loan doesn't require personal income documentation, it is still a mortgage that requires a strong financial foundation.

| Requirement | Typical DSCR Loan Guidelines |

|---|---|

| Credit Score | Minimum 620–660+ (Higher scores unlock better rates). |

| DSCR Ratio | 1.00 or higher is generally required, though some programs allow slightly less with compensating factors. |

| Down Payment | Typically 20% to 25% of the purchase price. |

| Cash Reserves | 3–12 months of the property’s PITIA (Principal, Interest, Taxes, Insurance, etc.) must be held in liquid assets. |

| Property Status | Must be a non-owner-occupied investment property. |

| Documentation | Appraisal (with Market Rent Analysis), Credit Report, and Bank Statements to prove reserves/down payment funds. |

📈 Rates and Costs

DSCR loans are Non-QM loans, meaning they carry a slightly higher risk for the lender. As a result, you should expect interest rates to be higher than those offered on conventional investment property mortgages.

Trade-Off: You are paying for speed, flexibility, and the ability to bypass restrictive DTI limits. For a cash-flowing property, the slightly higher rate is often worth the ability to close quickly and expand your portfolio.

Prepayment Penalty (PPP): Many DSCR loans include a prepayment penalty (often 1–5 years) to compensate the lender for the higher risk. Ensure you understand this term before closing.

🔑 DSCR Loan: A Must-Have Tool in Your Investor Toolkit

The DSCR loan is not just an alternative; it's a strategically superior financing option for serious real estate investors. It shifts the focus from your personal tax situation to the actual performance of the asset, enabling you to acquire more properties, execute cash-out refinances to secure capital, and streamline the entire underwriting process.

If your investment property's cash flow can cover its debts, this loan can help you unlock your next great deal with unprecedented speed and flexibility.

MORTGAGE ARTICLES

133 E. De La Guerra St. #59

Santa Barbara, CA 93101

Email: loans@mortgagewholesale.com

805-419-3319

NMLS: 380097

Copyright © 2025 Mortgage Wholesale - All Rights Reserved