Bank Statement Loans: Mortgages Without Tax Returns or W-2s

The Wholesale Advantage: Why Brokers Win for Bank Statement Loans

Bank Statement Mortgages are considered "Non-Qualified Mortgages" (Non-QM). Unlike standard loans (which are backed by Fannie Mae and Freddie Mac), Non-QM loans are offered by specialized wholesale lenders who set their own flexible guidelines.

A mortgage broker like Mortgage Wholesale is your gateway to this entire network of specialty lenders, giving you access to the most favorable loan terms available on the market.

1. Access to the Widest Range of Flexible Products

Traditional retail banks often offer only one or two rigid Bank Statement products. A wholesale broker, however, works with dozens of specialized Non-QM lenders who are highly competitive.

Custom-Fit Qualification: Brokers can shop your unique financial profile (e.g., 12 months vs. 24 months of statements, personal vs. business accounts) against all the top programs to find the one that maximizes your approved income.

Deep Lender Network: They have relationships with industry-leading wholesale lenders who design programs specifically for self-employed individuals with complex finances.

2. Maximized Buying Power & Low Down Payments

Wholesale lenders specializing in Bank Statement Loans offer some of the most aggressive terms in the industry, making homeownership more accessible and affordable:

High Loan Amounts: Wholesale lenders offering financing up to $10,000,000 for jumbo loans.

High LTV (Low Down Payment): Access programs that require as low as a 10% down payment (90% LTV) for purchase transactions.

Low FICO Scores: Get approved with credit scores down to 600-620 (often with a higher down payment).

3. The Best Rates Through Competition

Wholesale brokers are not bound to one bank's rates. They can shop your completed application to multiple competing wholesale lenders simultaneously.

This forced competition means you are more likely to secure the absolute lowest interest rate and the most competitive closing costs available for your specific credit and income profile, potentially saving you thousands over the life of the loan.

4. Expert Guidance on Complex Income Calculation

A Bank Statement Loan's approval hinges entirely on how your income is calculated. A skilled wholesale broker working with their non-qm lender know the nuances of these programs better than a general bank loan officer:

Optimizing Deposits: They know how to handle and document unusual deposits, transfers between business and personal accounts, and other factors to ensure your income is accurately and fully credited.

The Right Calculation Method: They can choose between different qualification options—such as a fixed expense factor (e.g., 50% deduction), a CPA-prepared Profit & Loss statement, or an analysis of net deposits—to pick the method that gives you the highest qualifying income.

In short, a top-rated mortgage broker utilizing the wholesale channel is your Non-QM specialist. They turn the traditionally frustrating process of self-employed mortgage lending into a streamlined, high-efficiency path to approval.

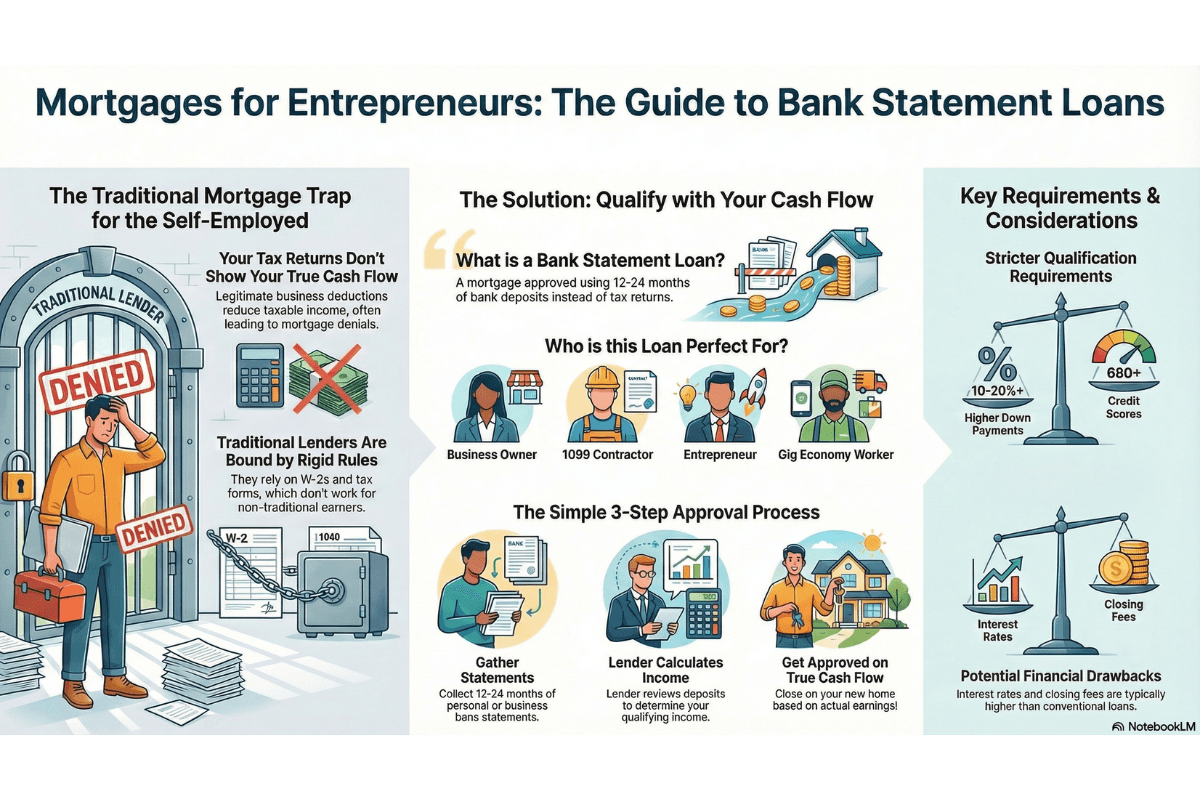

Are you a successful self-employed entrepreneur, business owner, or 1099 contractor who finds it impossible to qualify for a traditional mortgage? You're earning great money, but your savvy tax write-offs mean the "net income" on your tax return doesn't reflect your true cash flow. Traditional lenders, shackled by strict W-2 and tax return rules, often deny your application—even though you are financially strong.

The good news? There is a powerful, flexible solution designed for people like you: The Bank Statement Loan.

This guide breaks down exactly how this mortgage program works, who it’s perfect for, and the simple steps to get pre-approved for your next home.

What is a Bank Statement Loan?

A Bank Statement Loan is a type of Non-Qualified Mortgage (Non-QM) specifically designed for borrowers with non-traditional income documentation.

Instead of demanding two years of W-2s or IRS tax transcripts, the lender qualifies you based on the deposits and cash flow shown in your personal or business bank statements.

This approach allows lenders to see your real, day-to-day income without penalizing you for legitimate business deductions on your tax return.

Who Should Consider a Bank Statement Mortgage?

This loan program is the ideal path to homeownership for:

Self-Employed Business Owners: If you have high write-offs that minimize your taxable income, a Bank Statement Loan uses your gross deposits to qualify you for a higher loan amount.

1099 Independent Contractors & Freelancers: You can use your 1099 income and bank deposits instead of being forced to use your lower net income from tax filings.

Entrepreneurs with Multiple Revenue Streams: Whether you have consulting income, rental income, or multiple businesses, the loan can easily accommodate your complex financial picture.

Gig Economy Workers: Individuals who rely on consistent deposits from various sources can use the strength of their cash flow for qualification.

If you are tired of your tax deductions being a roadblock to your mortgage approval, this loan is the solution.

How Bank Statement Loans Work: A 3-Step Process

The process is straightforward, focusing on your financial stability through cash flow, not just tax forms.

Step 1: Gather Your Statements

You will need to provide either 12 or 24 consecutive months of bank statements. These can be from:

Personal Bank Accounts: The lender will analyze deposits, excluding transfers, to establish your average monthly income.

Business Bank Accounts: The lender will look at total business deposits and then apply a standard expense ratio (often 50%, but this varies by lender) to determine your qualifying net income. Example: If your average monthly deposits are $$15,000, and the expense ratio is 50%, your qualifying income is $$7,500/month.

Step 2: The Lender Calculates Your Qualifying Income

An in-house underwriter will meticulously review your statements to:

Average Deposits: Determine the consistent, average monthly income flowing into your account(s).

Apply Expense Ratio: For business accounts, they apply the pre-determined ratio (e.g., 50%) to arrive at your effective income for loan qualification.

Exclude Non-Income Items: They remove any large, non-income deposits, such as loan proceeds, inter-account transfers, or large one-time gifts.

Step 3: Approval Based on True Cash Flow

The lender will then use this calculated monthly income to determine your Debt-to-Income (DTI) ratio and your maximum buying power. This focuses on your real-world ability to repay the loan, often resulting in a higher approved mortgage amount than you would get with tax returns.

Key Requirements and Drawbacks to Know

While flexible, Bank Statement Loans are considered a higher-risk product, meaning they have a few stricter requirements compared to a conventional mortgage.

Requirements:

Credit Score: Typically requires a good to excellent credit score, often a minimum of 680–700+.

Down Payment: Down payment requirements are usually higher than for FHA or conventional loans, often starting at a minimum of 10%–20%.

Self-Employment History: You must have a minimum of two years of self-employment or 1099 contract work.

Reserves: Lenders often require several months of mortgage payments saved as cash reserves after closing.

Potential Drawbacks:

Higher Interest Rates: Because this is a Non-QM loan with alternative documentation, the interest rates tend to be higher than standard conventional loans.

Fees: Closing costs and fees may be slightly higher than traditional loans.

Potential Prepayment Penalty: Some Bank Statement Loans if they are for investment properties can carry a prepayment penalty if you refinance or sell the home within the first few years (this is lender-dependent, so always ask).

The Bottom Line: Your Path to Homeownership

For the successful self-employed borrower, the Bank Statement Loan program is the key that unlocks the door to homeownership. It’s a sophisticated financial product that finally recognizes that taxable income is not the same as spending power. If your business is thriving and your bank accounts show consistent, strong cash flow, you no longer have to be penalized by your tax strategy.

MORTGAGE ARTICLES

133 E. De La Guerra St. #59

Santa Barbara, CA 93101

Email: loans@mortgagewholesale.com

805-419-3319

NMLS: 380097

Copyright © 2025 Mortgage Wholesale - All Rights Reserved